×

Question 1:

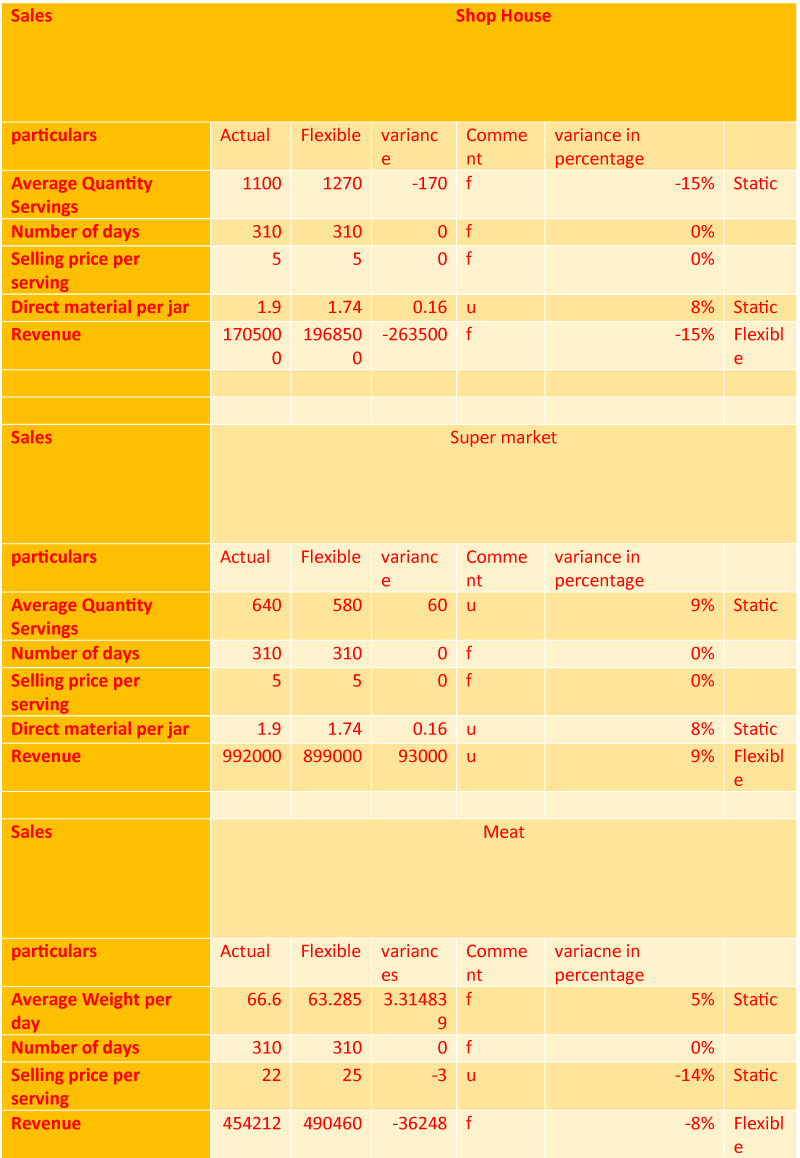

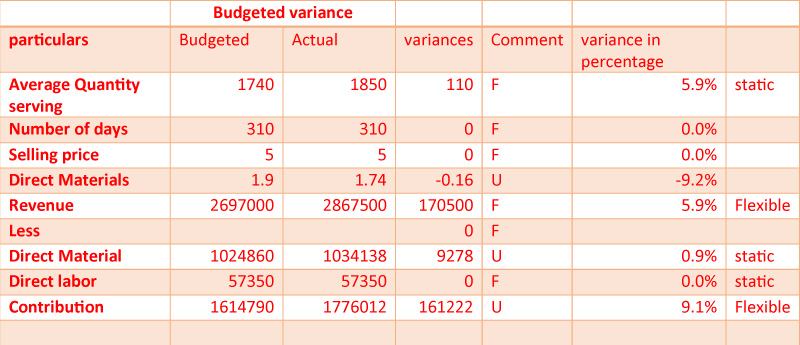

a) Computation of Flexible and Static Variance

In this section of the study, the discussion will highlight the various variance tools to estimate the organization`s performances.

Flexible variance:

A flexible budget is a budgetary tool to evaluate the performance of the budgeted amounts with the actual figures and flexes with the changes in volume or activities. The flexible budget can be calculated by multiplication of actual and budgeted consumption in budgeted costs (Vesty and Brooks, 2017).

Static variance:

A static variance is the measure of exact variance between the actual consumption and budgeted consumption at actual consumption rate (Tan and Low, 2017).

b) Preparation of flexible budget performance report

c) Potential problems associated with employs engagements when setting the budget.

A commonly agreed phenomenon that causes a serious problem in setting sales and other budgetary process is due to the employee engagements. Here, using the bottom-up approach will be influential in making adjustments regards to process various types of information processing depending on the environment from participation (Nimon, Shuck and Zigarmi, 2016). Therefore, input from the employees engaged in the sales will help in budget preparations. If the management can engage the sales employees in the budget-making process, then it will be a two-way benefit for the company. Firstly, the company could ascertain a potential budget for the future period. Secondly, the employees will have prior knowledge of the budget; this will make them efficient and their duties towards the organization. Employee engagement could be increased by the following processes:

Giving Individual Attention: This will increase the overall scope of efficiency of the company by different thought process.

Providing training and coaching: Adequate training and coaching will eventually increase the efficiency of the employee to deal with the real-life problems with adequate influence in making the budget and another essential process of the company (Robson et al., 2016).

Question 2:

Introduction:

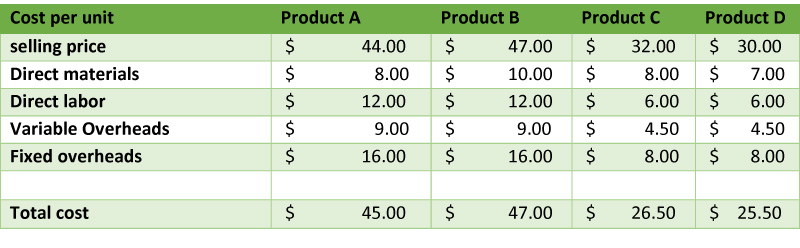

In the given case, Shining Ltd is manufacturing four different product from the same machinery. Currently, the company is evaluating all the function and resources available to lower the cost as well as to meet the increased demand. In the appease of this report, two potential proposals for product managements such as making overtime production which will increase the product cost and secondly importing product c from an overseas supplier. The effects of such are as follows.

Proposal 1:

In this option, the management wants to increase productivity by introducing additional production hours. By making additional production hours, the company can surely increase the supply of their offerings but this surly increase the cost of production as the company has to pay additional wages to the labours and eventually the variable cost will be increased proportionately. In that case, the total production price per unit is exceeding the total sales price (Davis et al., 2016). Therefore, this option is not validating the requirements of the organization. Increasing production is not the ultimate option. If the company is kept pace with the same sales price, then this proposal needs to be ignored. Though product C and Product b are remaining profitable.

Proposal 2:

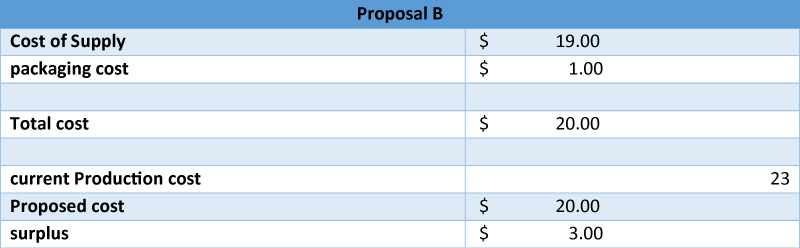

In this option the management has ascertained their production beyond the normal production limit as additional production in increasing the overall cost of the product and product A and Product B is considering costly compared to the sales price. In this option, the management is considering to import Product c from a foreign supplier which will cost amount $19 per units, including the transportation cost. Further, the company has to spend an additional $1 for the packaging and others. This option seems profitable as the second maximum production is made for Product C. if the management could arrange the same from external supplier with the same quality then, in that case, it could indulge the balance production hours in producing the other product is that product A, B and D (Kim et al., 2019). This will eliminate the additional working requirements and resulting the process less costly. Further, the cost of production of Product c seems to be costly compared to the total cost of importing it from external sources.

Recommendation:

In the given case, the management of Shining Ltd. should oblige with proposal two as this is effective in reducing the cost of product C. furthermore increase the outputs of other products without effecting the production cost. Therefore the company`s profitability will be increased by the low cost of Product C and incased production of Product A, B and D.

Conclusion:

In the contents of the report, the evaluation of the different proposal and their effectiveness in current scenarios. The qualitative and quantitative approaches will deliver the needs of the company`s evaluation process. In this case, a proposal for changes and their collateral effect is valuable in forming the decisions are identified.

SHN6023 : Mental Health, Resilience and Recovery Across the Life-course – Case Study Assignment

Read MoreBUS6009 : International Business Management – Written Case Report

Read MoreBUS6018 : PROJECT MANAGEMENT – PROJECT PLAN

Read MoreHCM4003 : Communication and Interprofessional Collaboration – Podcast

Read MoreQHO335 : Business Project – Critical evaluation of an organisation’s response during the cost-of-living crisis in the UK

Read MorePRM7006 : Management of Traditional Projects – PID Assignment

Read MoreBMA5108-20H : International Business – Strategic Evaluation

Read MoreCA5055 : Airline Revenue and Pricing Management – REPORT

Read MoreCA5056 Aviation Psychology and Human Factors Assignment brief

Read MoreHow can i assist with youGBEN5006 : Intrapreneurial Development – Portfolio

Read More